Annonse

When will the next economic crisis hit?

An important lesson from economic crises is that they are so distinct from each other.

Published

The coronavirus crisis in 2020 sent the world into what Norway's then-Minister of Finance Jan Tore Sanner called the greatest ever peacetime economic crisis in Norway (link in Norwegian). Several of our foremost economic experts forewarned a dark and gloomy future for the country.

Then the situation abruptly turned. Today, the Norwegian economy has completely recovered.

Very special crisis

The coronavirus crisis was a rather special economic crisis: it was caused by a virus.

Financial crises, banking crises and housing crash crises have been much more common.

Annonse

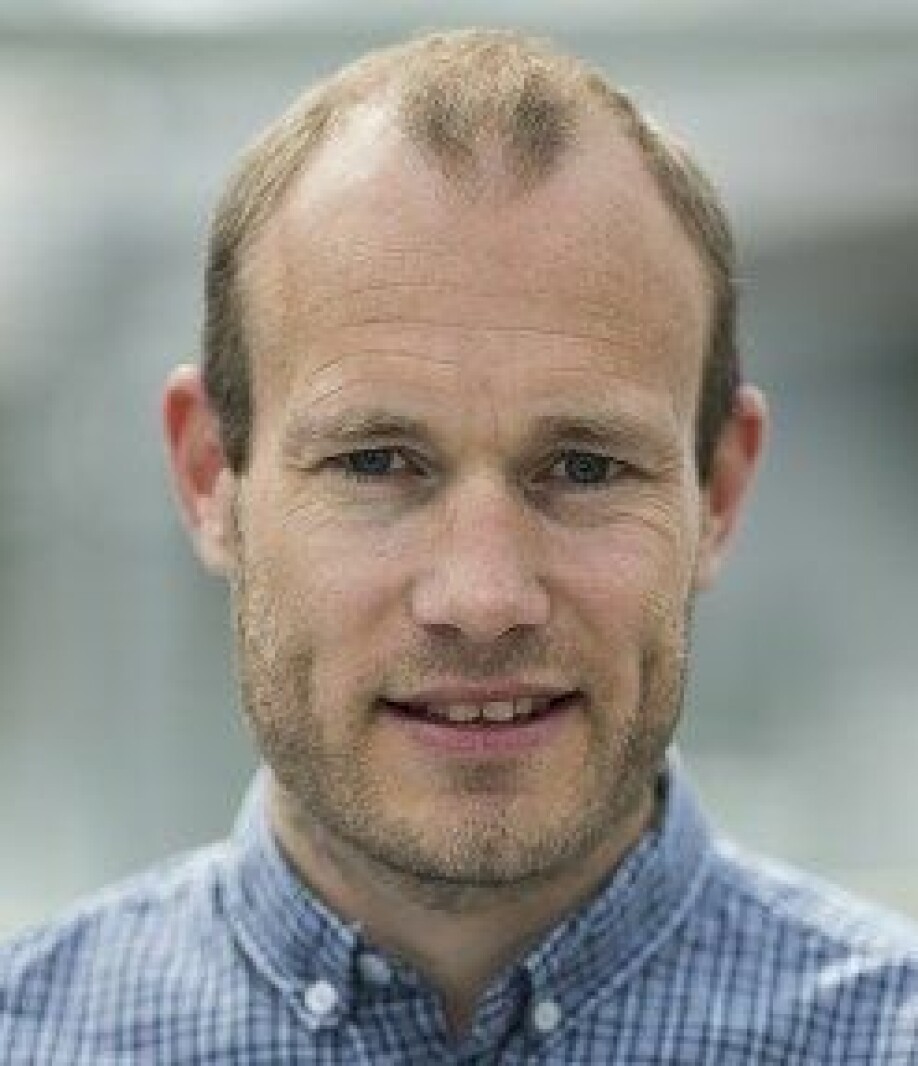

“Looking at the global financial crisis in 2008 and 2009, for example, its cause was that the financial industry in the USA and parts of Europe had developed in a way that couldn’t continue,” says Espen Ekberg, an economic historian at BI Norwegian Business School.

During the corona crisis in 2020, nothing had fundamentally failed in the international economy.

Experts completely wrong about corona crisis

The global economic crisis 13 years ago was created by a financial industry where several key players went off the rails in the battle to sell high-profit products – the contents of which only few buyers understood.

The Terra Securities scandal was a Norwegian offshoot in which several municipalities borrowed a lot of money and invested in various hedge funds, or “structured credit products” in finance lingo.

“Simply put, the financial crisis in 2008 and 2009 was caused by the financial industry itself,” says Ekberg.

“What ended up being called the Covid crisis in 2020 came about for completely different reasons. And if we go back to the banking crisis in Norway in the years between 1987 and 1992, this had yet another quite different triggering cause.”

“The banking crisis involved several Norwegian banks losing such large amounts on their loans that their equity was completely or partially lost. The banks would have gone bankrupt if the Norwegian state hadn’t intervened.”

Two years ago the Norwegian News Agency (link in Norwegian) wrote that historians could identify almost no worse economic crises than the one Norway was experiencing then. The Norwegian research foundation Fafo also reported that ‘this time Norway won’t be ready for the storm.’

How wrong one could be about the corona economic crisis.

Norwegian banks historically strong

Economic historian Ekberg believes it is worth noting how the financial industry reacted to this most recent crisis in 2020.

“This time, the financial industry proved to be both solid and energetic.”

Annonse

“Here in Norway, banks were able provide help in the form of debt deferrals to companies. Norwegian banks have also maintained their credit offering. They’ve helped a lot of companies keep their wheels turning,” Ekberg says.

The BI historian believes that the financial industry, with banks at the forefront, has in general remained steady through the Covid crisis.

He adds that Norwegian banks have probably never in their history been stronger than they are today.

Dangerously high debt levels

Economic crises are one of Ekberg’s specialities. He observes that despite the fact that these crises differ from each other and have somewhat different starting points, two important features typically lead to economic crises:

- The debt level skyrockets.

- The price of securities and housing increases dramatically.

“We’re experiencing both of these things right now,” the BI researcher says.

“The debt level is at an historic high. The price of shares is also really high, not least in the USA’s important stock market.”

“On top of that, the price of housing has risen a lot both in Norway and a number of other places in the world,” he says.

But these developments have one important factor in common: there is a lot more money in the world now.

Is there too much money now?

The enormous ‘money printing’ in the United States was supposed to help keep the wheels turning during the coronavirus.

“The question now is how effective this strategy has been. I can’t say whether it’s been right or wrong. But a lot of people in the field are worried that the spike in money supply has contributed to fueling share and real estate prices,” says Ekberg.

In short, this situation is about the US Federal Reserve buying (primarily) government bonds, enabling the central bank to distribute the new dollars it has issued and get them into people’s hands.

“Behind the money printing is a desire by the central bank to maintain economic activity. The question is whether this is now creating a bubble in the economy, with share prices climbing far too high,” says Ekberg.

“Money that was supposed to create new start-ups and support businesses is instead contributing to Tesla’s and Apple's shares rising to sky-high levels.”

Doesn’t like doomsday prophets

When the next economic crisis hits, Ekberg fears that high debt and high share and housing prices may be the triggering factors.

“Rapid debt build-up and high debt have been shown to create financial crises multiple times throughout history.”

“When we look at the increase in housing prices in Norway, the USA and several other countries, it’s easy to imagine that something similar could happen again. But saying anything for sure is really difficult,” says Ekberg.

Ekberg notes that he himself has little interest in economists and researchers who throw out predictions to the media that we’re now facing a new economic crisis.

“Sometimes they get it right. Then we’re reminded of it again and again afterwards. If they’re wrong, we never hear about it again,” he says.

“But often they’re wrong.”

Can high interest rates create problems?

John Arngrim Hunnes is an associate professor at the University of Agder (UiA). He too has researched economic crises. A few years ago, Hunnes and his colleague Ola Grytten analysed Norwegian economic crises over the last 80 years.

“You’re posing a difficult question when you ask a researcher about the next economic crisis, because then you’re asking me to look into the future,” Hunnes says.

Hunnes concurs that predictions about the future should not be one of the tasks of economic historians.

“Almost all economic crises have proved difficult to give advance warning about,” he says.

What worries the UiA researcher the most at the moment, however, is whether a new sharp rise in interest rates is appropriate right now. He worries about the ability of households to handle such an interest rate increase.

Another interesting feature of the times is that we’re starting to see high inflation figures, especially in the United States, Hunnes says.

“This is a signal that interest rates should rise sharply, which would create a challenge for households with a lot of debt.”

Crises follow good years

Hunnes reminds us that crises often follow several years of good economic times.

“Crises often hit when people are feeling optimistic.”

“People are looking forward to the future and invest more and more at ever higher prices,” he says.

“Share prices and home prices are rising without there being any fundamental merit in the price increase. The underlying values don’t match the high prices.”

In Hunnes’ experience, crises like this have generally been difficult to see coming.

Psychology is part of the picture.

“A lot has to do with people's expectations for the future based on whether the economy will pick up or slow down,” he says.

Can afford to lose money on stocks

Hunnes also points out that a large drop in share prices and a crisis in the stock market do not necessarily generate a strong impact on the real economy.

“People who are active in stock investing generally have a greater ability to lose more money than other people do.”

“Most people will only experience an economic crisis if they themselves notice it in their everyday lives. That’s when an economic crisis becomes really serious for society,” says Hunnes.

Translated by: Ingrid P. Nuse

References:

Ola Honningdal Grytten and Arngrim Hunnes: An anatomy of financial crises in Norway, 1830–2010. Financial History Review, 2014.

Björn Audunn Blöndal: Historiens verste finanskriser (History's worst financial crises). Finansforbundet, 2021.

Sverre August Christensen: Hva kan vi lære av 100 år med økonomiske kriser? (What can we learn from 100 years of economic crises?). article on the BI website, 2020.

———

Read the Norwegian version of this article at forskning.no